Growth Up, Jobs Down: India’s Dilemma

By Haresh Jhala

Unemployment climbs as small business closures expose the cracks in India’s growth story

India’s headline growth numbers tell one story. The ground tells another. When the Periodic Labour Force Survey quietly records a national unemployment rate of 5.5% — and millions simply stop looking for work — the applause for GDP milestones begins to sound hollow. The real crisis is not visible in stock indices or export figures. It is unfolding in shuttered workshops, unpaid invoices, and idle hands across every district of this vast, restless nation.

1. The Ground Reality: Unemployment Data That Cannot Be Wished Away

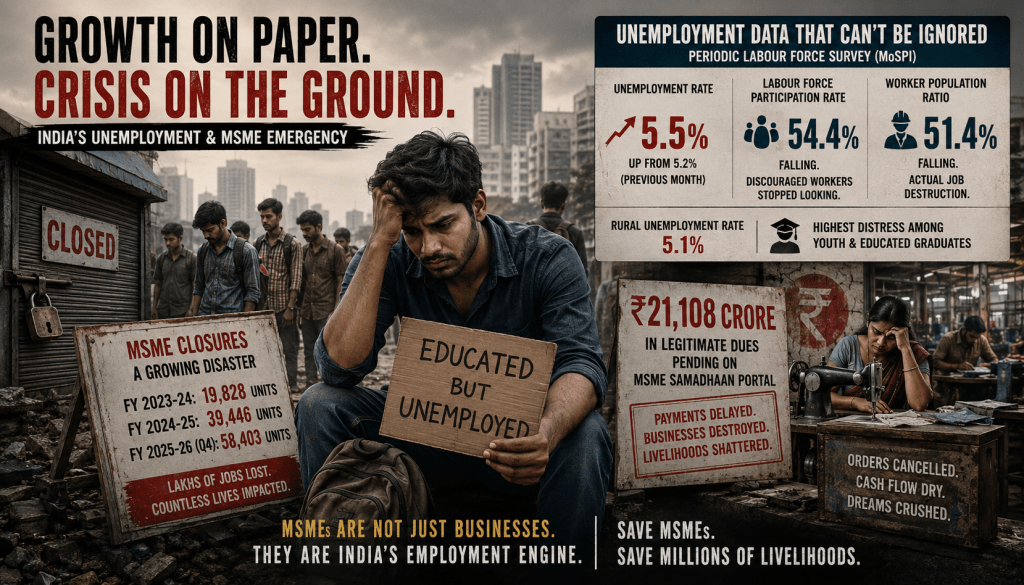

The latest data released by the Ministry of Statistics and Programme Implementation (MoSPI) through its Periodic Labour Force Survey offers no comfort to those who insist India’s economy is firing on all cylinders. The national unemployment rate has climbed to 5.5%, up from 5.2% in the previous month. That single percentage-point shift, easily dismissed as statistical noise, conceals a structural emergency playing out in three distinct ways.

First, the Labour Force Participation Rate (LFPR) has fallen to 54.4%. This is not merely a data point — it signals a growing mass of discouraged workers: people who have stopped seeking employment altogether, having concluded the search is futile. When citizens withdraw from the labour market out of despair rather than choice, no unemployment figure can fully capture the human damage beneath it.

Second, the Worker Population Ratio (WPR) has slipped to 51.4% — a direct reflection of actual job destruction, not seasonal fluctuation or demographic adjustment. Fewer working-age Indians are employed today than a month ago. That is the unvarnished reality.

Third, the distress is concentrated in rural India. Rural unemployment has surged to 5.1%, as an agrarian economy already under stress absorbs displaced industrial workers for whom no urban alternatives exist. The countryside, perpetually asked to bear the weight of economic transition, is once again shouldering burdens it cannot sustain indefinitely.

Beneath these headline numbers lies a structural trap rapidly becoming permanent. According to MoSPI’s own findings, a disproportionate share of India’s unemployed are educated youth — graduates who invested years and family savings into university degrees, only to find the economy has stopped producing the mid-tier formal employment their qualifications were meant to unlock. For those under 25, the open joblessness rate is a crisis hiding in plain sight within government data.

2. The Broken Engine: MSMEs Are Not a Policy Category — They Are the Economy

Any honest analysis of India’s employment crisis must begin here: Micro, Small, and Medium Enterprises contribute over 30% of GDP, approximately 45% of manufacturing output, and nearly 80% of all non-farm employment, according to the Ministry of MSME’s own published figures. No other sector comes close to matching that contribution to the daily livelihoods of ordinary Indians.

Large corporations may dominate boardroom conversations and stock market headlines. But MSMEs feed families. They employ the semi-skilled worker in Surat, the craftsman in Moradabad, the garment stitcher in Tiruppur, the food processor in Pune. They distribute income not upward into shareholder accounts but horizontally — across rural talukas, semi-urban clusters, and marginalised communities that no large conglomerate has ever seriously committed to reaching at scale.

When this sector weakens, the consequences are not merely economic. They are social. MSMEs represent the primary ladder of upward mobility for India’s lower-middle class and first-generation entrepreneurs. They are where a rural migrant finds his first formal wage. Where a woman runs a home-based unit and achieves a measure of financial independence unavailable to her mother’s generation. Where a school dropout becomes an employer of ten within a decade.

Crush MSMEs, and you do not merely reduce GDP. You remove the ladder entirely. India’s celebrated demographic dividend — the largest young working-age population on earth — becomes not an asset but an accelerant for social instability when the employment base that sustains it is systematically hollowed out.

3. The Carnage: What the Udyam Portal’s Numbers Actually Mean

The scale of MSME closures is now formally documented in Parliamentary records. Data submitted through the Udyam Portal — the government’s own official MSME registration platform — reveals a trajectory that demands urgent policy attention:

- FY 2023–24: 19,828 units formally closed

- FY 2024–25: 39,446 units closed — a near-doubling in a single year

- FY 2025–26 (as of Q4): 58,403 units — an accelerating wave with no sign of reversal

These are not casual closures or routine business exits. Each unit represents a proprietor’s life savings, a family’s livelihood, and the wages of multiple workers who now have nowhere to go. The formal layoff count within the micro-enterprise tier alone runs into lakhs of documented cases — and that figure excludes the vastly larger informal workforce that disappears from records without a trace when a small unit shuts.

The primary driver of this carnage is a chronic cash-flow crisis of the most preventable kind. Over ₹21,108 crore in legitimate business dues sits frozen on the MSME Samadhaan portal — money owed to micro-enterprises by large corporate buyers who routinely delay payments for 90, 120, even 180 days. The MSME supplier cannot pay its workers, cannot service its bank loans, cannot purchase raw materials for the next order cycle — and eventually pulls down the shutter. Not because the business model failed. Because a larger, more powerful entity simply refused to pay what it legally owes, on time.

This is not a market failure. This is a power failure — the unchecked ability of large capital to choke small capital without meaningful consequence, despite the legal framework of Section 43B(h) of the Income Tax Act existing precisely to prevent it.

4. The GDP Illusion: India’s K-Shaped Growth Model Exposed

India’s GDP growth rate continues to attract favourable international commentary. The numbers, however, require a far more uncomfortable reading.

The economy is locked into a K-shaped trajectory — a divergence in which two entirely different economic realities coexist within a single national statistic:

Upper tier: Large corporates, capital-intensive industries, high-end IT services and financial sector — recording strong profits, rising equity valuations, and accelerating automation investment.

Lower tier: Labour-intensive MSMEs, daily wage earners, the informal sector, and rural markets — experiencing mass closures, erosion of real wages, and rising household debt burdens.

GDP grows because capital is producing more value per unit. But this is not the same as saying human welfare is improving across the population. When a factory automates its assembly lines and retrenches a significant portion of its workforce, output per unit rises and GDP benefits. Those workers do not appear in the headline growth figure — only in unemployment statistics that receive considerably less celebration at investment summits.

India is not growing poorer as a nation. It is growing more unequal with remarkable speed. And inequality of this depth and velocity does not remain an economic condition for long. It becomes a political and social condition — one that no infrastructure spend, export incentive, or scheme allocation can quietly absorb.

5. The Corporate and IT Sector: Why the Old Promise Has Collapsed

For two decades, India’s economic policy narrative rested on a comfortable assumption: that large corporations and the expanding software services sector would absorb surplus labour as industrialisation deepened. That assumption is now demonstrably false, and it is past time to say so plainly.

Large enterprises are not expanding headcount. They are deepening capital intensity — choosing automation, artificial intelligence, and contract labour over permanent employment. This is rational behaviour for an individual firm. It is a catastrophe when it becomes the aggregate direction of an economy that needs to generate employment for tens of millions of young people entering the workforce every year.

The IT and technology services sector — once positioned as India’s employment engine — has quietly shifted to a model in which each successive generation of technology requires fewer human operators, not more. Generative AI tools are replacing entry-level coding, data processing, and back-office functions at a speed that the industry’s hiring pipelines have not adjusted to. Mid-level professionals face structural redundancy. Fresh graduates face hiring freezes. The sector that absorbed hundreds of thousands of engineering graduates annually is now retrenching, not expanding.

No policy narrative can survive sustained contact with these structural facts. The employment model that India’s growth story was built upon has changed — and the adjustment in policy thinking has not kept pace.

6. Broken Policy Foundations: When Scheme Design Defies Economic Logic

The government’s headline policy response to the employment crisis has been the Pradhan Mantri Viksit Bharat Rozgar Yojana (PMVBRY) — an allocation of ₹1 lakh crore designed to subsidise corporate hiring costs and generate one crore formal jobs annually.

According to Ministry of Labour data and Parliamentary disclosures, the programme achieved enrolment of approximately 4.4 lakh workers — a small fraction of its stated annual target.

This is not merely an implementation failure. It is a fundamental design flaw rooted in a misreading of how private enterprise makes hiring decisions. Companies do not hire because the government subsidises payroll costs. They hire because demand exists for their products and services. When purchasing power across the mass market is suppressed — because the MSMEs that employ the majority of India’s non-farm workforce have collapsed — the corporate sector has no rational incentive to expand headcount, subsidy or not. You cannot subsidise your way to employment generation in a demand-constrained economy.

Similarly, Production-Linked Incentive (PLI) schemes have attracted genuine investment into electronics, pharmaceuticals, and advanced manufacturing — achievements that deserve acknowledgement. But the facilities built under PLI are, by design, highly automated. They generate significant capital output and export value while creating a fraction of the direct employment that a traditional labour-intensive cluster of equivalent investment would produce. A semiconductor plant and a garment cluster of identical capital outlay are not equivalent employment generators. Policy must reckon honestly with that distinction rather than presenting PLI success as an employment story it structurally cannot be.

Policy cannot simultaneously celebrate capital-intensive industrialisation and claim to be solving a labour-absorption crisis. These are contradictory objectives. The employment data makes clear which objective is currently prevailing.

Leave a comment