MSME Briefing Entrepreneurship Desk

The opportunity, risks and supplier roadmap every MSME should know

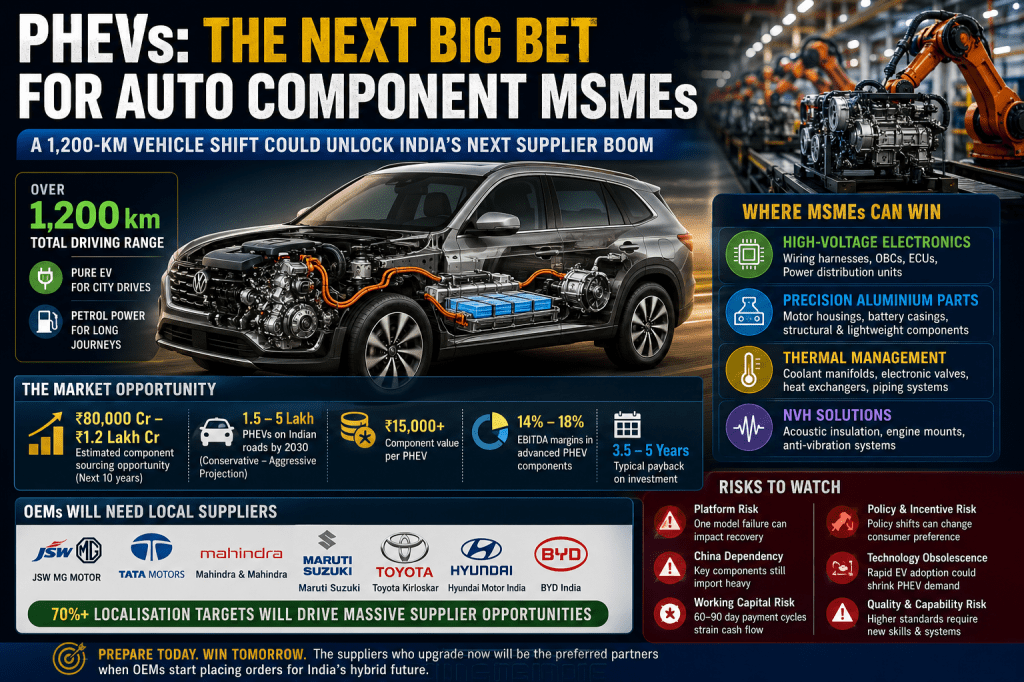

For years, India’s automotive component industry has been trapped between two realities. The traditional Internal Combustion Engine (ICE) business still generates cash, but its long-term future is increasingly uncertain. Pure Electric Vehicles (EVs) promise growth, yet many MSMEs remain hesitant to invest heavily in technologies that are still evolving. Now a third pathway is emerging. Plug-In Hybrid Electric Vehicles (PHEVs) may become the bridge between today’s automotive ecosystem and tomorrow’s electric future, creating a fresh wave of opportunities for component manufacturers, electronics suppliers, foundries, machine shops and engineering entrepreneurs willing to move before OEM procurement teams begin placing large-scale orders.

The Deadlock Facing India’s Auto MSMEs

Across industrial clusters in Rajkot, Sanand, Ahmedabad, Chakan, Pune, Aurangabad, Hosur, Coimbatore, Faridabad and Gurugram, thousands of component manufacturers face the same question:

Should we continue investing in ICE components, or should we bet aggressively on EVs?

Neither answer appears comfortable.

Traditional engine components face increasing pressure from emission regulations, fuel efficiency norms and changing consumer preferences.

Meanwhile, pure EVs eliminate many components that have supported MSME growth for decades, including engine assemblies, fuel systems, exhaust systems and numerous precision-machined parts.

For many entrepreneurs, this uncertainty has delayed investment decisions.

That hesitation may soon become costly.

Why PHEVs Could Change the Game

A modern Plug-In Hybrid Electric Vehicle is not simply a petrol vehicle with a battery.

Nor is it a conventional hybrid.

It is effectively two propulsion systems operating inside one vehicle.

A typical next-generation PHEV combines:

- A large battery pack (18-30 kWh)

- High-voltage power electronics

- Electric traction motors

- Battery cooling systems

- Electronic control modules

- High-voltage wiring harnesses

- Thermal management systems

- A highly efficient petrol range-extender engine

- Fuel delivery systems

- NVH control systems

For vehicle manufacturers, this complexity increases engineering challenges.

For suppliers, it increases sourcing opportunities.

Unlike a pure EV, which removes significant mechanical content, a PHEV often creates demand across both conventional and advanced component categories.

That makes it particularly attractive for Indian MSMEs seeking a gradual transition rather than a complete technological leap.

The OEM Signal MSMEs Should Not Ignore

The strongest indicator is not the vehicle itself.

It is the localisation requirement.

Automakers cannot indefinitely rely on imported assemblies if they wish to remain cost competitive in India.

Manufacturers including JSW MG Motor, Tata Motors, Mahindra & Mahindra, Maruti Suzuki, Toyota Kirloskar, Hyundai Motor India and BYD will ultimately require increasing levels of local sourcing.

This creates opportunities not only for large Tier-1 suppliers such as Motherson, Bharat Forge, Uno Minda, Lumax, Sona BLW, Endurance Technologies, Suprajit Engineering, Talbros, Sansera Engineering and Pricol, but also for hundreds of Tier-2 and Tier-3 suppliers embedded across India’s industrial clusters.

The question is not whether localisation will happen.

The question is which MSMEs will be ready when RFQs begin arriving.

Where the Real Opportunities May Emerge

1. High-Voltage Wiring and Electronics

Potential Investment: ₹4-8 Crore

Likely Demand Areas:

- High-voltage cable assemblies

- Battery junction boxes

- Power distribution units

- Electronic control modules

- Battery management enclosures

- On-board charging systems

Companies such as Napino Auto & Electronics, Vecmocon Technologies, Celectric Mobility and Griden Power have already demonstrated the direction in which automotive electronics is moving.

For MSMEs with electrical assembly expertise, this may represent one of the fastest-growing opportunities.

2. Precision Aluminium Manufacturing

Potential Investment: ₹3.5-7 Crore

Future demand is likely for:

- Motor housings

- Battery casings

- Structural aluminium components

- Cooling plate assemblies

- Lightweight engine components

Clusters such as Rajkot, Sanand, Coimbatore and Aurangabad already possess many of the machining and casting capabilities required to participate.

3. Thermal Management Systems

Potential Investment: ₹2-5 Crore

This segment remains underappreciated.

A PHEV must manage temperatures for:

- Batteries

- Electric motors

- Power electronics

- Internal combustion engines

Expected demand includes:

- Coolant manifolds

- Electronic valves

- Thermal modules

- Heat exchangers

- Specialised piping systems

Many OEMs are expected to localise these products rapidly because transportation costs make imports less attractive.

4. Noise, Vibration and Harshness (NVH)

Potential Investment: ₹1-3 Crore

PHEVs create a unique engineering challenge.

A vehicle may operate silently on battery power before the petrol engine suddenly activates.

This transition must remain smooth and refined.

Potential opportunities include:

- Acoustic insulation

- Engine mounts

- Anti-vibration assemblies

- Sound damping materials

Margins in this category are often higher than traditional metal components.

The Numbers Entrepreneurs Should Study

Industry analysts estimate that hybrid and plug-in hybrid vehicle demand could grow significantly during the next decade as India balances electrification goals with infrastructure realities.

Even if PHEVs capture only a modest share of India’s annual passenger vehicle market, the associated component sourcing opportunity could exceed ₹80,000 crore to ₹1.2 lakh crore over the coming decade.

A supplier winning business worth approximately ₹15,000 per vehicle on a programme producing 24,000 units annually could generate:

Annual Revenue Potential: ₹36 Crore

Advanced electrification components frequently achieve EBITDA margins of 14% to 18%, substantially above many traditional automotive categories.

The Risks Nobody Should Ignore

Platform Risk

A supplier investing heavily in tooling for one unsuccessful vehicle programme may struggle to recover capital.

China Dependency Risk

Many critical electronic components remain heavily dependent on Chinese supply chains.

Geopolitical disruptions could create sudden shortages.

Localisation Delay Risk

OEM announcements do not always translate into immediate sourcing orders.

Timelines can slip.

Technology Obsolescence Risk

If battery costs fall faster than expected and charging infrastructure expands rapidly, pure EVs could accelerate beyond current projections.

Working Capital Risk

The biggest threat to MSMEs is often not technology but cash flow.

Automotive payment cycles of 60-90 days can create severe financial strain during ramp-up.

Capability Risk

Manufacturers accustomed to conventional machining may underestimate the quality, traceability and testing standards required for electrified vehicles.

Final Thoughts

Every major industrial shift creates winners and spectators.

India’s PHEV opportunity is not merely about vehicles. It is about a supply-chain transition that may open a temporary but potentially lucrative window for manufacturers willing to upgrade capabilities before the market reaches scale.

The entrepreneurs who wait for certainty may eventually find themselves competing in shrinking legacy markets.

The entrepreneurs who begin preparing today may become preferred suppliers in India’s next automotive chapter.

The factory floor is already in place.

The question is whether the next phase of growth will happen on it—or somewhere else.

Leave a comment