By Haresh Jhala

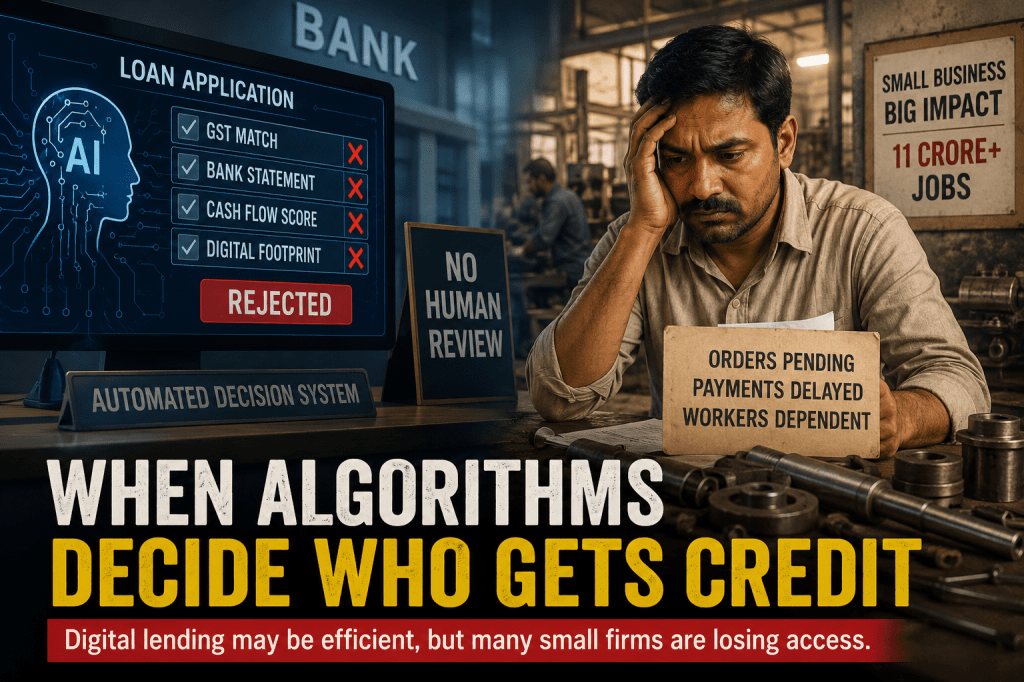

Loan values are rising, but the number of MSMEs getting credit is falling.

India’s banking system has a success story to tell. Outstanding credit to MSMEs has crossed ₹46 lakh crore, posting a healthy 12.8% year-on-year growth.

But beneath the headline number lies a worrying reality.

Between December 2025 and April 2026, MSME credit growth slowed sharply to just 3.1%, compared with 9.7% during the same period a year earlier. More alarmingly, the number of active MSME loan accounts fell by 3.5%.

Think about that for a moment.

The total amount of money in the system is still growing, yet fewer businesses are actually receiving it. The money is increasing. The borrowers are disappearing.

The biggest casualties appear to be micro enterprises. Credit to micro units contracted by 3.1% during the same period, while early signs of financial stress among these businesses continued to rise. Manufacturing and trade, two sectors that account for the majority of MSME activity and employment, also witnessed a significant slowdown in credit expansion.

This raises an uncomfortable question.

Are banks becoming better at managing risk while becoming worse at supporting entrepreneurship?

Reality Check: Who Drives India’s Economy?

MSME Sector

- More than 6.3 crore enterprises

- Contributes around 30% of GDP

- Generates over 11 crore jobs

- Accounts for nearly 45% of manufacturing output

- Receives only about 12-14% of total institutional bank credit

Corporate India

- A few thousand large listed and unlisted firms

- Contributes roughly 20-22% of GDP

- Employs less than 2 crore people

- Commands nearly 30-35% of formal bank credit

The sector creating the most jobs continues to receive a disproportionately smaller share of institutional finance.

The slowdown cannot be blamed entirely on technology. Global uncertainties, trade disruptions and tighter risk management have all made lenders more cautious.

However, the growing reliance on automated underwriting systems deserves closer examination.

Modern lending models increasingly depend on GST filings, bank statement analytics, tax records and algorithm-driven risk assessments. These systems are efficient, fast and scalable. For businesses with clean, consistent digital records, they work remarkably well.

The problem is that entrepreneurship rarely follows perfect algorithms.

A small manufacturer may face delayed payments from a large customer. A local exporter may experience temporary cash-flow pressure because of shipment delays. A seasonal business may witness fluctuations that look suspicious to software but are perfectly normal to an experienced banker.

Computers can detect a variance.

They cannot always understand the reason behind it.

As lenders seek safety, capital naturally gravitates toward borrowers with stronger documentation, larger balance sheets and lower perceived risk. Recent data indicates that lending is increasingly concentrated among the safest borrower categories, while smaller enterprises struggle to maintain access to working capital.

The decline in active loan accounts suggests exactly that.

For large corporates, such challenges are manageable. They employ finance teams, compliance specialists and external consultants. They have access to credit ratings, capital markets and multiple funding channels.

The typical MSME owner has none of these advantages.

Often, the entrepreneur is simultaneously the owner, production manager, marketer and finance head. A single accountant handles compliance. Yet these businesses are increasingly expected to satisfy the same data-driven scrutiny imposed by sophisticated lending systems.

That creates a dangerous risk for the economy.

When formal credit becomes difficult to access, businesses do not stop operating. They postpone expansion, delay hiring, reduce production or turn to expensive informal lenders. Over time, this weakens manufacturing competitiveness, suppresses job creation and reduces the ability of small firms to participate in India’s growth story.

The irony is striking.

India wants more manufacturing, more exports and more employment. Yet the very sector expected to deliver those outcomes is finding credit harder to access.

Technology should remain an important part of banking. Faster approvals, digital processing and collateral-free lending are positive reforms. But technology should assist judgment, not replace it.

A flagged application should trigger review, not automatic exclusion. Minor cash-flow disruptions should be evaluated in context. Branch-level MSME specialists should retain the authority to apply human judgment where algorithms cannot.

Because a small business is more than a data trail.

It is a factory floor, a payroll, a supply chain and a livelihood.

If India wants its MSMEs to lead the next phase of economic growth, the banking system must remember a simple truth: the objective of lending is not merely to avoid risk. It is to finance productive enterprise.

And sometimes, that requires a banker—not just an algorithm.

Leave a comment